A deeper dive into understanding defensive allocations

In this article, we dive into the core of fixed income, focusing on three critical concepts: duration, credit spreads, and default risk. We know that finance terms (particularly in fixed income) can feel like a foreign language if you aren’t immersed in this world daily. To help bridge the gap, we’ve put together this ‘Bonds 101’ guide to explain these concepts and why they matter for your money.

What is a Bond?

A bond is just a loan. When you buy a bond, you are lending money to a company or a government (the ‘issuer’). They promise to pay you interest along the way and return the ‘principal’ at the end of the loan (‘maturity’). You will also hear the term ‘credit’, which is generally used to refer to company loans.

There are two main risks with lending money to companies:

- Interest Rate Risk: The risk that market rates go up, making your bond less valuable.

- Default Risk: The risk that the borrower goes broke and can’t pay you back.

1. Interest Rate Risk

Bond prices and market interest rates have an ‘inverse’ relationship, like a see-saw. When market interest rates rise, the value of existing bonds goes down, and vice versa.

For example:

You buy a 1-year bond paying 6% interest for $100. The next day, market rates increase to 6.5%.

- The Problem: No-one will buy your bond that pays 6% interest for $100, because they can get 6.5% interest elsewhere in the market.

- The Solution: To sell your bond, you must lower your price to around $99.50. This price discount compensates for the 0.5% interest ‘gap’, so the new buyer effectively earns the same 6.5% return at maturity.

However, it is important to understand that price movements are generally just a timing factor – if you hold your bond to maturity and the issuer does not default, the issuer will pay you back the principal.

The Impact of Time

The length of the loan acts as a multiplier for this risk. To elaborate on the previous example:

- With a 1-Year Bond – the buyer only needs to be compensated for one-year of lower interest, so the price drop is small.

- With a 20-Year Bond – the buyer would have a ‘bad deal’ of 0.5% less interest paid every year for two decades, so the price has to drop significantly to compensate for the lower interest rate.

How We Measure this risk: Duration

Duration is a ‘sensitivity score’ for a bond. It tells you exactly how much the price will move if interest rates change by 1%. In approximate terms:

- If a bond has a duration of 5, a 1% rise in rates = a 5% fall in price.

- If a bond has a duration of 10, a 1% rise in rates = a 10% fall in price.

- Rule of Thumb: The longer the bond’s life, the higher its duration (and its interest rate risk).

When to think about adding duration

When interest rates (yields) rise to high absolute levels, there is inevitably a higher chance they will fall in the future.

As we explained in the ‘see-saw’ example earlier, when interest rates fall, the price of bonds go up. By adding ‘duration’ in this situation, you are positioning the portfolio to benefit from that price increase.

Interest rates typically fall when the economy hits a rough patch. It is important to understand that interest rates don’t always move in tandem at different maturities. The central bank rate can fall whilst the 10 year government bond yield might not (or it might move by a lesser amount). Nevertheless, there is some embedded link between the short and long end of the curve. To benefit from duration, you need the longer end of the yield curve to fall (remember, duration measures typically increase as the maturity of bonds increase).

When the stock market is expensive and there is uncertainty around economic growth, higher duration bonds can act as a cushion in the event that interest rates need to fall to protect the economy. If the stock market (your ‘growth’ investments) gets bumpy, the rising value of your bonds can help offset those losses to an extent. The chart below shows you have a better chance of adding value via duration if you purchase toward the top of the chart.

2. Default Risk

Another important concept to understand in fixed income is default risk and credit spreads:

- Default Risk: The chance the issuer won’t give you your money back. Unlike interest rate risk discussed above, this is what we call ‘permanent impairment’.

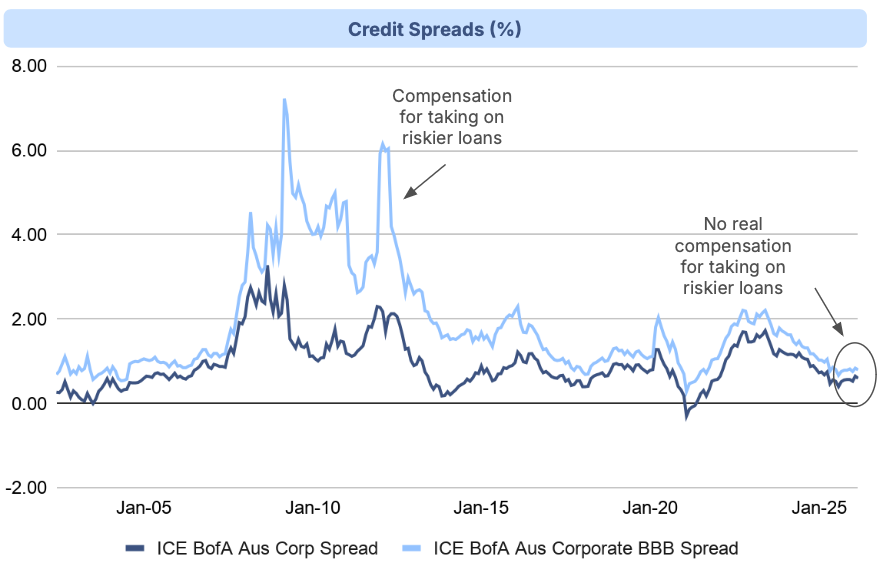

- Credit Spread: This is the extra interest rate that you are paid for taking on the risk of loaning to a company instead of a ‘safe’ government. Think of it as a risk bonus.

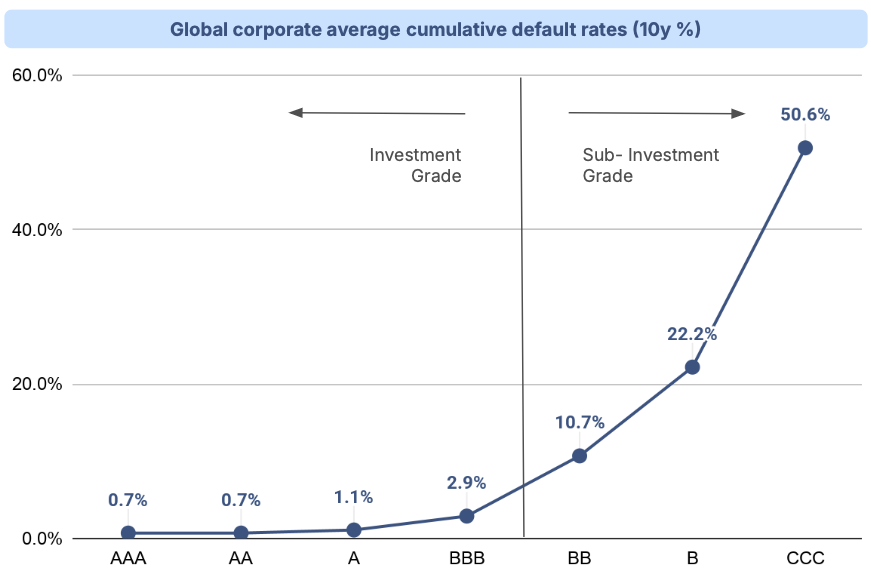

There are different types of bonds, which carry different amounts of default risk. The term ‘investment grade’ is used to describe bonds from safe governments and corporations which have very low default risk (risk of not paying your money back). The term ‘sub-investment grade’ is used to describe companies that have higher debt levels, are often smaller in size and have a much higher default risk. These investment or sub-investment grade ratings are assigned to bonds by credit rating agencies such as Moody’s, S&P or Fitch.

As with all investments, you only want to take on more risk if you are being paid a sufficiently higher return to do so.

Any loans categorised by the credit rating agencies as AAA to BBB are considered investment grade; anything below BBB is considered sub-investment grade (see the chart below). The chance of a borrower failing rises dramatically once you cross that divide.

As you can see in the chart below, there is a ‘cliff’ in safety:

- BBB (The lowest ‘investment grade’ rating): Has a 2.9% chance of default.

- BB (The first ‘sub-investment grade’ rating): Has a 10.7% chance of default.

That is ~4x increase in default risk for a very small increase in interest. If the market isn’t going to pay us a significant credit spread (or ‘risk bonus’) to jump off that cliff, we simply won’t be there.

In summary, navigating fixed income requires a clear understanding of its core return drivers and risks. The term of a loan, the general interest rate environment (duration) and creditworthiness of a corporation (credit spread / default risk) all play a role in the future performance of fixed income assets. By strategically positioning these exposures, investors can ensure their fixed income allocation acts as a true defensive asset, providing stability and buffer when it matters most!